The volume of leased logistics and industrial spaces in the first nine months of last year amounted to approximately 600,000 m2, 15% less than in the same period in 2023, and new contracts accounted for 58% of the total volume traded. Separately, in the third quarter, 175,000 m2 were traded, a level comparable to the period July-September 2023. The trend is slightly downward, after about 225,000 m2 were contracted in the second quarter of 2024, and almost 200,000 m2 in the first three months. Contract renewals accumulated 42% of the volume traded, having a significant share. At the end of 2024, the national stock of logistics and industrial spaces was of approximately 7.9 million m2, a surface divided equally between Bucharest and the rest of the country.

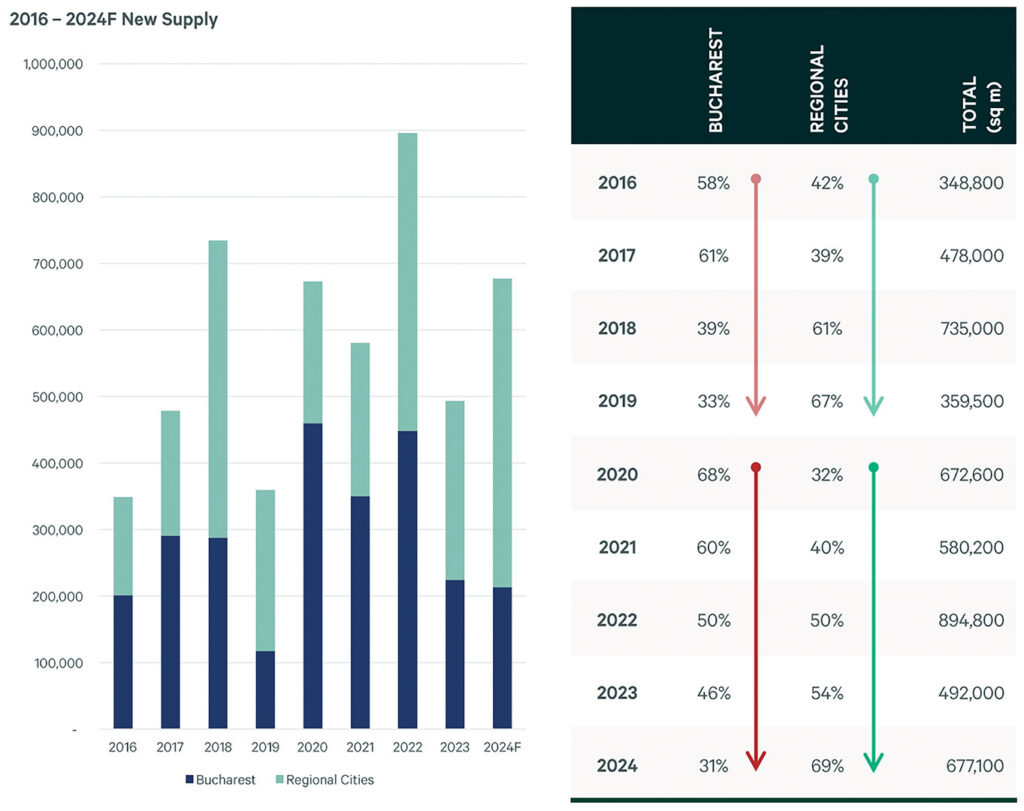

In a difficult and uncertain economic environment, tenants of industrial and logistics spaces in Romania analyzed very carefully in 2024 the existing options and tried to maximize the costs of a possible move. Developers continued to deliver new projects, so that in the third quarter a total of over 170,000 m2 was completed, of which the most relevant is the 53,500 m2 expansion of VGP Brașov for the client Inter Cars. In total, in the first nine months, projects of approximately 375,000 m2 were delivered and by the end of 2024 the total volume was expected to increase at approximately 600,000 m2 of new spaces. Under these conditions, last year ended with a national stock of 7.9 million m2, 10% more than in the previous year.

Bucharest remains the preferred destination for companies renting logistics and storage spaces, with almost half of the traded volume, while Timișoara, Ploiești and Cluj were the most dynamic secondary markets. On the other hand, the Capital also has the most vacant spaces.

The largest transactions in the industrial segment in 2024 (and the largest overall) were the two in which Globalworth sold its industrial space portfolio to the two largest owners in the market, namely CTP and WDP. Thus, CTP took over from Globalworth approximately 268,000 m2 of industrial space in Timișoara, Arad, Oradea, Pitești and Bucharest, for approximately 168 million euros. At the same time, WDP, in turn, bought from Globalworth approximately 136,000 m2 of industrial space and adjacent land in Bucharest, Constanța and Târgu Mureș, for approximately 110 million euros.

Among the other important transactions concluded in the first three quarters we can mention: VAT’s pre-lease of 20,900 m2 in VGP Park Arad, Deichmann’s pre-contract of 20,000 m2 in ELI Park 3 Bucharest, as well as Tenneco’s 19,000 m2 transaction in Ploiești, following a sale & leaseback agreement with WDP. Maravet also pre-leased 11,000 m2 in WDP Park Baia Mare, and Polish retailer Zabka signed a pre-lease of 10,000 m2 in MLP Bucharest West (new entries on the Romanian market). Especially in the third quarter there was the pre-lease of a 9,500 sqm for the production of lighting and surge protection equipment by a German company in CTPark Pitești, as well as the contracting of 6,000 m2 by the distributor Alliance Healthcare at WDP Park Dragomirești , according to the latest report by Cushman & Wakefield Echinox.

”Even in a context of decreasing demand compared to the previous year, the Romanian logistics and industrial space market remains resilient, supported by a representative volume of new leases and expansion projects. With a very high occupancy rate of over 95% and the prudent development of new projects, the logistics sector in Romania remains an essential and healthy engine of economic development and a barometer of industrial activity. The prospects are optimistic, because in the medium- and long-term Romania has good development potential in both the distribution and production sectors, the latter being on an upward trend in the last three years”, said Rodica Târcavu, Partner Industrial Agency Cushman & Wakefield Echinox.

The main concerns of real estate investors are now the level of interest rates, along with economic uncertainty, consumption contraction and inflation. This is evident from the ”Real Estate Investors Sentiment Barometer” study, conducted by Cushman & Wakefield Echinox together with some of the most important real estate investors and developers in Romania, who hold a cumulative real estate portfolio here valued at over ten billion euros and a share of approximately 50% of the local market. Despite the existing challenges, most of the responding investors want to expand their portfolios, especially in the industrial segment, and although the Capital represents for many the main target for new investments, secondary cities are also emerging as attractive destinations in the coming period.

Romania is very competitive in respect of rent costs

Retail, e-commerce and logistics remain the main demand generators, accounting for over 50% of the traded volume. Manufacturing has a higher percentage than last year, at around 35%, and it is believed that there is room for further development and evolution.

Compared to the rest of the CEE countries, Romania has the most competitive rent level, a vacancy rate equal to the regional average and we are in 2nd place after Poland in terms of newly delivered spaces, explained Călin Badea, I&L consultant at CBRE Romania. ”The market in our country has increased in complexity, with a visible transition towards production with higher added value, because of the increasingly skilled labor force and shortening of supply chains through infrastructure development and Schengen area access. At the same time, we are no longer as competitive as before for production with low added value, mainly due to the increase in wages. These factors may contribute to an increase in the rental costs in 2025, if developers continue their conservative approach. The potential for new projects in 2025 comes from both the industrial and logistics sectors. At the moment, the main sources of investors for next year are China, Turkey, Poland, Germany and the United States. Unfortunately, we are seeing a decrease in demand from European automotive component companies present in Romania.”

Important transactions of VGP Romania in 2024

VGP Romania started in 2024 the construction of the third building in VGP Park Bucharest North (A3). Called Building A, it will have an area of 25,950 m2 and already has two important clients who have rented a total of 8,158 m2.

VGP Park Bucharest is developed on 250,000 m2, with a total leasable area of approximately 120,000 m2, divided into four buildings.

Among the important transactions of VGP in 2024, it is worth mentioning the delivery of the 20,000 m2 warehouse to Continental Tires, which will carry out its tire storage operations within the eighth building within VGP Park Timișoara. The building covers a total area of 32,768 m2, of which 8,265 m2 are still available for rent. Also in VGP Park Timișoara, 4,580 m2 were leased to Rondocarton Romania. The park covers a total area of 349,098 m2 and includes eight completed buildings, with flexible units and areas starting from 1,500 m2.

In September 2024, VAT Romania started construction of a new factory in VGP Park Arad. The factory will occupy 21,000 m2 and will include – in addition to the production unit – offices and a canteen for employees. The building will comply with BREEAM Excellent standards and will be ready in the second quarter of 2025, with full operationalization scheduled for early 2026.

VGP has started construction works on the extension of building B in VGP Park Brașov. In the first phase, 13,813 m2 will be added to the existing 20,920 m2 space, to meet the growing demand for modern logistics spaces in the area. Of the additional 13,813 m2, 20.6% are already leased. With a total area of approximately 320,000 m2, VGP Park Brașov offers 140,000 m2 of space available for lease. Three buildings already delivered cover 55,000 m2.

WDP wants to invest 1.5 billion euros in key markets

In 2024, WDP completed several projects totaling 80,000 m2. The portfolio continues to grow steadily, delivering developments for clients such as Pirelli, Formfleks-Erkurt Holding, Trico Wipers and Taparo. The company owns approximately 2 million m2 of logistics and industrial space in all major urban centers in Romania.

WDP operates an urban logistics cluster near Bucharest, which covers an area of 300,000 m2, of which 100,000 m2 is built.

In 2024, the Belgian developer announced the expansion of the warehouse capacity in Ștefăneștii de Jos for the food retailer Metro. The project includes the development of a new temperature-controlled warehouse (refrigerated and frozen) of approximately 15,000 m2. Metro has signed a 10-year lease commitment for this warehouse, with a total investment of approximately 20 million euros, with delivery planned for the third quarter of 2025. Furthermore, WDP has acquired a portfolio of leasable warehouses and a plot of land for future developments of over 300,000 m2 of gross leasable area (GLA). The total investment amounts to approximately 110 million euros.

NewCold, one of the world’s largest automated cold storage operators, has acquired a 9-hectare plot of land in northern Bucharest from WDP. This step marks NewCold’s expansion into Eastern Europe, given the growing demand for automated and efficient storage solutions in the region.

In the first nine months of 2024, WDP achieved a strong investment volume of +600 million euros, of which approximately 100 million euros in Q3, with an average return of 7%. These investments were distributed across all operations of the company, including developments, acquisitions, land reserves and energy projects, excluding land acquisitions and energy investments. Approximately 75% of these were directed to Western Europe.

Romania, CTP’s second largest market

Romania is CTP’s second largest market, with over 2.6 million m2 of Class A industrial and logistics space in over 15 cities, including Arad, Brașov, Bucharest, Caransebeș, Cluj-Napoca, Craiova, Deva, Oradea, Pitești, Sibiu, Târgu Mureș, Timișoara, Ineu and Salonta. The real estate developer acquired a 270,000 m2 industrial portfolio and 30 hectares of land in six key locations in the country from Globalworth last year.

Among the most important transactions completed in 2024 is the renewal of the contract with Cummins Generator Technologies in CTPark Craiova, where the manufacturing company operates on 17,000 m2 of the total leasable area of 59,000 m2 of the industrial park. Located along the European roads E70 and E79, facilitating fast connections to Bucharest and Pitești, CTPark Craiova offers versatile facilities for production, cross-docking, warehousing, logistics and R&D.

CTP has delivered 23,000 m2 of the CTPark Arad West project, and another 20,000 m2 are ready for fit-out works by tenant companies. The recently completed space is 12 m high and offers state-of-the-art logistics and distribution facilities, currently leased by Leoni Wiring Systems Arad, Delfingen, HUF Romania and BNB. CTPark Arad West was to obtain the BREEAM Excellent sustainability certification.

Launched in January 2024, the LPP group’s distribution center, located in CTPark Bucharest West, has been expanded by another 42,000 m2, reaching a total area of 91,000 m2. The unit supplies LPP brand stores, as well as two fulfillment centers in Romania dedicated to managing online orders in the region (Bulgaria, Hungary, Croatia, Macedonia, Serbia and Greece), with a storage capacity of up to 800,000 boxes.

In addition, in CTPark Bucharest West, the real estate developer, launched the dynamic CTBox project, aimed at small and medium-sized enterprises (SMEs), through which it offers flexible units of 500-600 m2 for rent. The unique configuration facilitates interaction with customers, offering SMEs visibility and growth opportunities similar to the benefits of co-working spaces for start-ups. The first tenant of the CTBox building is Profi, which opened a new supermarket within it, improving comfort for employees and the local community.

CTPark Bucharest West covers 855,000 m2 and includes the Clubhaus, a multifunctional center offering facilities such as a cafeteria, supermarket, amphitheater, meeting rooms, outdoor exercise areas and a medical office.

It is also worth mentioning the lease of 4,500 m2 in CTPark Deva by FAN Courier, this transaction bringing the total area occupied by FAN Courier in CTP parks to 10,000 m2 (after the warehouses in CTPark Sibiu East and CTPark Craiova East). Cargo-partner also leased another 7,800 m2 from CTP in CTPark Cluj, reaching a total of 28,000 m2 leased in Romania, and e-commerce logistics provider HelpShip leased 5,300 m2 within CTPark Oradea Cargo Terminal, the first industrial park with an air terminal for freight transport.

Other landmark transactions in 2024

Among the largest transactions concluded in 2024 are the sale-leaseback of 19,000 m2 of Tenneco’s premises in Ploiești to WDP, as well as the lease of 19,000 m2 by Yusen Logistics in CTPark Bucharest. This is followed by the pre-lease of 11,000 m2 concluded by Maravet within WDP Park Baia Mare and the lease agreement signed by Drim Daniel Distribuție for a 10,000 m2 warehouse space in MLP București Vest.

The American manufacturer Crane ChemPharma & Energy leased 3,000 m2 in Industrial Park Arad. Developed by Oresa Industra, the new industrial park is a premium location in Arad, completed in 2024, spanning 33,000 m2. Oresa Industra has consolidated itself in Iași as a major player in the industrial and logistics market. In 2023, it delivered 10,000 m2 of class A logistics space within Industra Park Iași, increasing the total leasable area of the park to 35,000 m2. Oresa Industra’s total portfolio amounts to 77,000 m2, and the Swedish company has projects in various stages of development, totaling 65,000 m2.

Construction costs remain a major challenge for the developers of industrial facilities. While some materials have seen price declines, others continue to rise. In addition, total construction costs are also influenced by external factors, such as rising energy prices and pressure on construction wages. These trends have kept the construction cost index at a high level, suggesting that, overall, prices have not completely stabilized. However, although the rent has been influenced in the direction of growth, it did not increase directly proportional to the construction costs. ”Considering that there are construction sites open almost all over the country and even tertiary cities are starting to appear on the map of new developments, we expect the market to continue to be quite dynamic, prices to remain relatively constant and new projects to continue to appear, both in terms of logistical developments and rental requests”, said Daniel Cautis, managing Partner Dunwell RO.

In Czech Republic, Slovakia, Romania, Hungary and Serbia there are about 2.2 million m2 of industrial and logistics spaces under construction, of which almost half are in the Czech Republic, points out Andrei Bentea, from iO Partners. Romania represents about 17% of what is under construction in the region. ”In general, the same halls can accommodate both logistics/storage or light production, depending on demand. Of course, the logistics/storage area still has a higher share compared to the production area (this is also because production units with very specific or restrictive requirements are generally owned by the occupants, as it would be difficult for a developer to rent someone else’s building in the event of the tenant leaving, unless the latter assumes a long-term or very long-term rental contract). But, at a regional level, we have seen a higher demand for renting production spaces this year, especially in the Czech Republic and Romania.” For example, Nokian Tires opened in 2024 a plant in Oradea, and the pharmaceutical company STADA inaugurated a new drug factory in Turda. There are quite a few companies prospecting Romania for new production units, including from sectors that have been poorly represented so far, for example the military industry, where Rheinmetal will develop a new powder factory in Victoria, Brașov County.

Positive dynamic of the industrial and logistics market

However, the industrial and logistics market has a positive dynamic – experts say – with significant growth prospects, but is influenced by high volatility in construction costs. In such a context, careful budget planning and a flexible strategy become essential for investors and developers to remain competitive and profitable in the long term.

The transition to sustainability and digitalization is stimulating investments in IT solutions, artificial intelligence, electric vehicles and green energy. On the other hand, traditional sectors such as conventional industrial production, physical retail and certain branches of classic transport are showing signs of decline. In particular, the automotive production/logistics segment is affected by several challenges, which have led to a slowdown in production in many European regions, including Romania.

”Regarding the European logistics market, the slowdown in the activity of some automotive companies in Europe could open up opportunities for Asian logistics companies, especially those collaborating with Chinese automakers. They are gaining ground in the European market, where sales of electric vehicles manufactured in China are constantly growing. In this context, logistics chains should be adapted to support the flows of goods from China to Europe, which could generate investments in logistics infrastructure in Romania, given the country’s strategic position.

Global geopolitical and economic uncertainties are causing companies to rethink supply chains, which could accelerate the diversification of suppliers and the attraction of new players from Asia. Thus, although the traditional European automotive sector is going through a difficult period, new dynamics are emerging that could transform Romania into a logistics hub for Chinese automakers expanding their presence in European markets”, said Rodica Târcavu.

72% of retailers are betting on larger surfaces in physical stores

The European Retail Occupier Survey 2024, conducted by CBRE, revealed that 71% of retailers who plan to expand their physical store network intend to do so in markets where they are already present. The study included responses from over 60 global retailers, with a network of stores totaling over 130,000 locations.

There was an increased preference for larger retail spaces, with 72% of respondents planning to expand their store size, up from just 26% in 2022. This trend is prevalent among fashion and athleisure brands in capitals and large cities. In the luxury sector, owning own stores is among the preferences of respondents, over renting them, however it remains predominant for the mass market, with 84% of respondents stating that they do not plan to buy stores.

In terms of preferred formats for future stores, retail parks are dominant, with 45% of respondents choosing them as locations for future stores. From a digital perspective, retailers are in the search and learning phase before implementing technological solutions. 61% of respondents indicated that they are exploring the possibilities offered by Artificial Intelligence (AI), but only 25% have already implemented these solutions.

ESG standards are gaining importance in the retail sector, according to the CBRE study, which shows that 6 in 10 retailers consider the ”green features” of buildings an advantage in leasing negotiations for the next three years. This represents an increase of 45% compared to 2022, clear evidence that such contracts, benefiting the environment, promise to become increasingly common.

Physical stores, overall, continue to be an essential component of retailers’ strategies, with 97% of respondents recognizing their importance. There is also a consensus on the efficiency of physical stores, which outperform online retail in terms of consumer engagement, cross-selling, overall effectiveness of sales strategies, as well as in introducing new products and attracting new customers.